Buy the Gold Miners?

Atlas Pulse Gold Report; Issue 74

We know there’s still a bubble in many parts of the stockmarket, and inflation may cool, but it won’t disappear. Whenever the economy starts to recover, it will resurface. Hold onto your gold.

Highlights

- Macro: Tightening to slow

- Valuation: Fair value returns

- Flows: Peak selling is behind us

- Technicals: The junior gold miners look good

MACRO

Another 0.75% hike by the Fed was well received by the gold price. It’s funny how the low in gold occurred back in 2015, just as the hikes were about to begin. Despite the popular view that gold hates hikes, the rally from $1,057 demonstrates there is more to it.

Gold withstands the rate hike

The message from the market, rightly or wrongly, is that the upward pressure on rates is behind us, the economy will cool, and inflation will soften. I’m sure that’s true to some extent, but what is clear is how a rise in the trend rate of inflation has played a bigger role since the 2015-low than interest rates.

Total inflation since 2015 has been 25%

Actual inflation is one thing, but the markets are always looking ahead. Inflation expectations jumped, albeit slightly, on the rate hike. The message here is that the Fed will fall short of containing inflation. The market still expects 3.4% annualised inflation over the next two years. With the last CPI print at 9.1% for last year, this does seem a little hopeful.

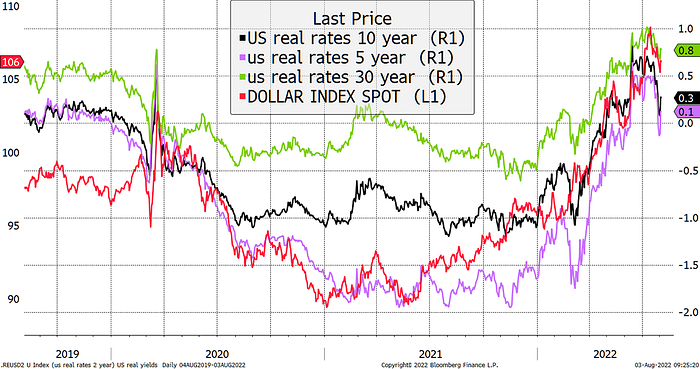

Fair value hit by real rate spike

But with cooling commodity prices, lower inflation is inevitable. This has been supportive for the bond market, which has seen real yields (rates less inflation) fall. That has helped to soften the dollar, and as we all know, gold loves a weaker dollar.

Real rates peak which softens the dollar

The good news is that gold has returned to fair value. The fair value swing has been extraordinary this year. It started at $2,100 in January, fell to $1,800, and then surged to $2,200, which was an all-time high. The price was right not to follow, as fair value subsequently fell to $1,600. Today, price and fair value are realigned.

A choppy rates environment has seen big moves in gold’s fair value

This highlights the importance of the increasingly volatile landscape for rates markets in influencing the gold price. What gold investors must not forget is that the 1.3% inflation reported for June alone is permanently added to the fair value of gold. And at current prices, gold will once again act as an efficient inflation hedge.

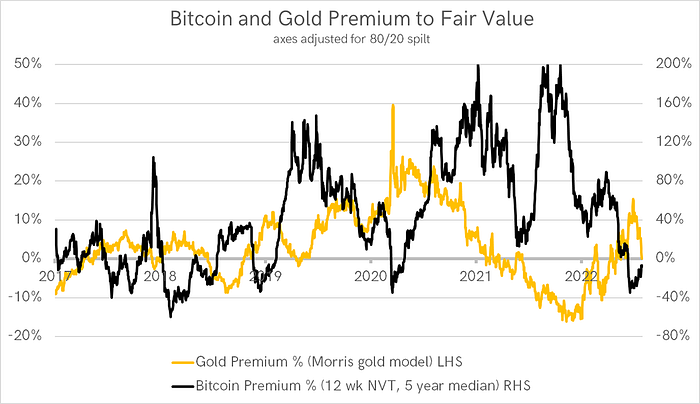

Talking of efficient inflation hedges, I remind you that gold is a risk-off asset. You can never expect it to shoot to a meaningful premium during the good times. The two occasions when gold shot to a premium occurred in 2011 and 2020, both when the global economy really was about to implode.

As always, the money printers came to the rescue. Gold retreated, and risky assets surged. There is no better example of this than bitcoin. Whenever investors are willing to pay a premium for gold, they are unwilling to pay up for bitcoin and vice versa.

The remarkable counter-cyclicality of gold and bitcoin

The ByteTree BOLD Index blends these assets on a risk-adjusted basis, roughly 80% gold and 20% bitcoin. It is remarkable how this combination has been such an efficient inflation hedge since 2020. Neither in isolation have been quite so timely.

ByteTree BOLD1 Index has been an efficient inflation hedge

I was asked by Dr Peter Warburton whether BOLD1 could be expected to generate a real and an absolute return. I replied here, and I believe it can, and will.

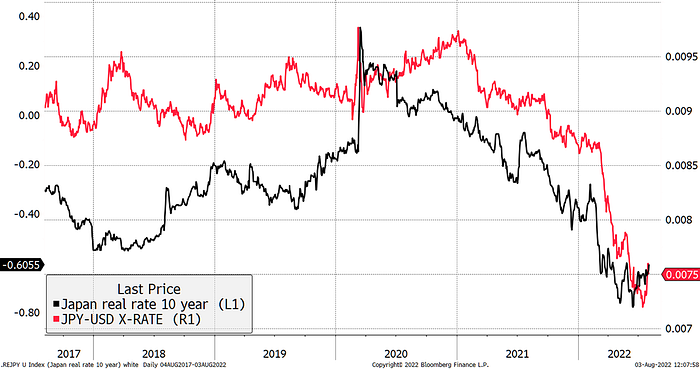

There’s one more thing on the macro, which is too good to miss. The Japanese yen has been falling this year, despite having consistently lower inflation than elsewhere. The reason is their refusal to hike rates, as they believed inflation would pass, which has seen investors sell the yen.

As inflation rose, Japanese real rates dropped into negative territory and dragged down the yen. Now that Japanese inflation is softening, real rates are rising, and the yen has turned up.

The yen was dragged down by falling real rates

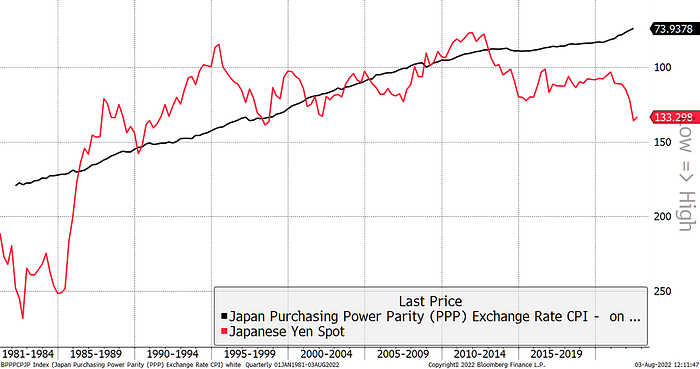

So far, this is no big deal as currencies rise and fall all the time. However, what has come to light is the extent of the yen’s structural undervaluation. Over the years, it has hovered around purchasing power parity, despite periodic deviations. In 1982, the yen was 35% undervalued against PPP and is currently a record 45%.

…while the yen remains deeply undervalued

The great yen rallies have often occurred during disinflationary moves, such as in the mid-1980s and during the 2008 financial crisis.

To have an inflation hedge to cover off risk-on and risk-off, you simply embrace BOLD1. But if you want to add a deflationary hedge into the mix, then look no further than adding the yen, as it has the potential to surge. Maybe I should launch the BOLDY index.

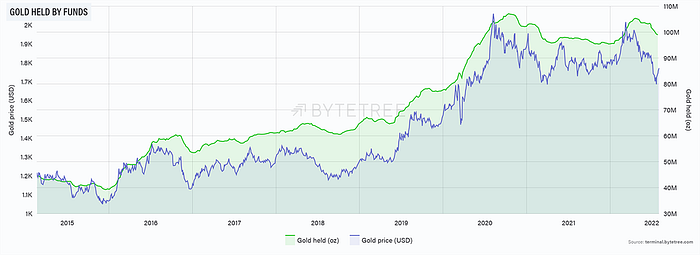

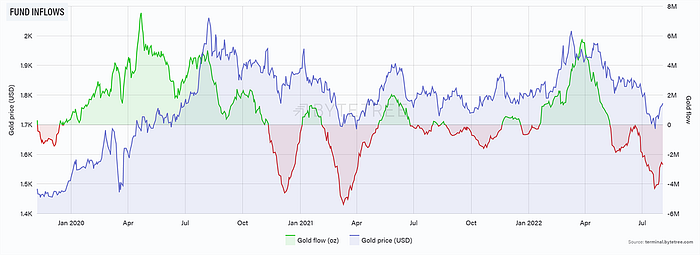

GOLD FLOWS

I remind you that we track gold ETF flow data on ByteTree Terminal, which is free to view. It shows that the outflows since April seem to be slowing.

Selling pressure eases on gold ETFs

The flows haven’t yet turned up, but the rate of change has. That implies better times ahead, or at least less downward pressure on the gold price.

Rate of change improves

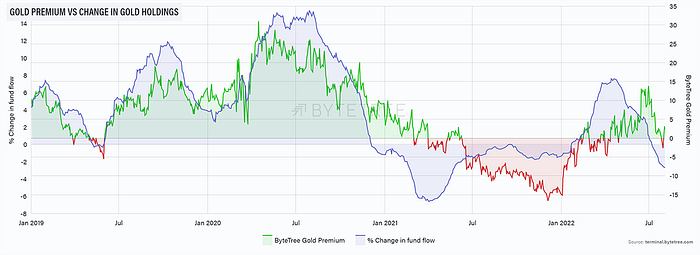

It is quite something how ETF flows seem to explain the shifts between gold premiums and discounts. Very clearly, heavy buying from 2019 to mid-2020 caused the gold price to overshoot to the upside, just as the selling drove the discount earlier this year. With the price back at fair value and the selling easing, the risks of holding gold have fallen dramatically.

The madness of crowds

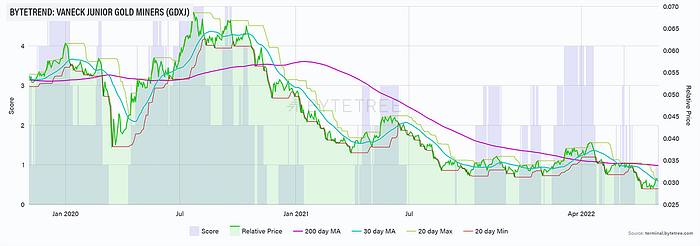

Buy the miners?

We have recently launched ByteTrend for over 300 equity ETFs. It is designed for data junkies to measure relative strength across the different equity themes. So far, you can measure the world in terms of my favourite index, BOLD1. We will soon be adding US dollars, along with various equity indices. Have a play, but I warn you, it is addictive.

Today, I couldn’t help but notice two ETFs that improved their trend versus BOLD1, which is hard to beat. One was the junior miners, GDXJ.

GDXJ jumps to 2 stars in BOLD

We have a scoring system that helps make sense of this, but in simple terms, the market leaders have 5-star trends, while the dogs have 0-star trends. Currently, most 5-stars are in the US, and most 0-stars are in the emerging markets. It’s a handy tool to identify the market leadership and the daily changes.

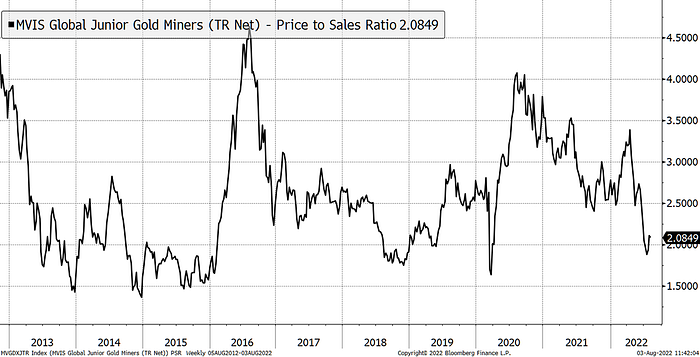

I’m never one to get too excited about a 2-star trend, as seen in GDXJ, but valuations are low enough while the gold price appears to be underpinned. In valuation terms, GDXJ is half the price of mid-2020, when investors couldn’t get enough of the gold miners. Now would be a better time for sure.

Junior miners back into cheap territory

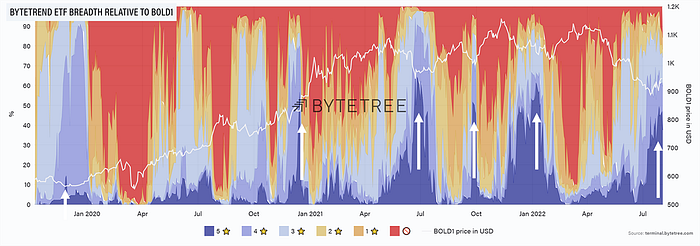

For the artists among you, we also have a breadth chart. It shows the number of ETFs that are outperforming BOLD1. Currently, it is quite high at around 50%, which is down to the recent fall in bitcoin. That can be seen by the spike in blue. Most of the time, there hasn’t been much blue, and the chart is dominated by red skies. That means BOLD1 is beating the 300 equity ETFs. I did say BOLD1 was hard to beat.

A timely entry point for BOLD

The blue spikes never seem to last for long, and then BOLD1 is back. It turns out that blue spikes have been good entry points. With bitcoin and gold back at fair value, that makes sense.

Gold with a yield

Finally, I wanted to highlight the work being done by Keith Weiner, founder of Monetary Metals, whose business issues gold bonds. I think more people in the gold world should be aware of his work. This plug is unpaid.

Monetary Metals is a different kind of gold company. Conventional gold businesses buy and sell gold. But Monetary Metals pays interest on gold. If conventional gold companies are like currency exchanges, this company is like a bank. They pay interest by leasing and lending it to businesses that use gold productively, such as jewellers, refiners and miners. They argue that gold is money and that the world took a wrong turn when governments forced people to stop using it. They are on a mission to build a bottom-up free-market gold standard. You can read more about this is an article he wrote.

You can follow Keith on Twitter, @RealKeithWeiner.

SUMMARY

The stockmarket reminds me of the summer of 2008. Many believed the worst was already priced in, only for Lehman to go bust a couple of months later. It is a reminder that the big moves are normally down to events. What could the next event be?

We know there’s still a bubble in many parts of the stockmarket, and inflation may cool, but it won’t disappear. Whenever the economy starts to recover, it will resurface. Hold onto your gold.

Thank you for reading Atlas Pulse.

If you wish to receive Atlas Pulse, then please subscribe to the ByteTree mailing list.

This article was written by Charlie Morris, Co-Founder and Chief Investment Officer at ByteTree. The article has been cross-posted from our website, originally published on 3 August 2022.

Visit ByteTree Terminal for Bitcoin on-chain data tracked in real-time. We also track Ethereum, Gold, and Silver Fund Flows.

Subscribe to our mailing list for free weekly updates.